How have the coronavirus lockdowns affected you?

Has the pandemic changed your strategy or approach to property investing?

Has the pandemic changed your strategy or approach to property investing?

Are you considering moving to live in a different location because of COVID-19?

These are only some of the Covid-19 related questions we recently asked 1,700 Australian property investors and would-be investors in our annual Property Investment Sentiment Survey conducted by Yahoo Finance and Property Update, and some of the answers were enlightening.

Running since 2011, our survey offers rich and vibrant insights into how property consumer trends and sentiments have changed over time.

A surprising result this year was that while only 12.4% of the respondents said their household finances had worsened because of the pandemic, in other words, most Australian households have noticed no real change or an improvement to their family finances, yet only 55.2% believe now is a good time to invest in residential real estate.

However, 24.7% of respondents plan to buy a new home in 2022 (up a little from 24% last year and 20% the year before.)

This is no surprise Covid has made us realise that our homes are more than just a place to live, but now they’re where we often work, work out, and spend most of our days.

You can download the full survey findings by clicking here, but for the moment let’s look at some of the survey highlights related to Covid 19.

Are you considering moving to live in a different location because of Covid19?

While 82.6% of the respondents were not considering living elsewhere, 6.2% considered moving to Queensland, while 5% thought regional Australia would offer a better lifestyle.

Do you believe now is a good time to invest in residential property?

Last year 74% of those surveyed believed it was a good time to invest in real estate, and they were right – property values have increased by more than 20% in many locations around Australia over the last 12 months.

Respondents to this year’s survey were less confident that now is a good time to invest in property (55.2%) and that’s most likely because of those significant increases in property values leaving many people wondering if it’s too late to get him to the market.

Respondents to the survey saw this as the best time to invest in property for a long time,

However, investors are optimistic about our property markets.

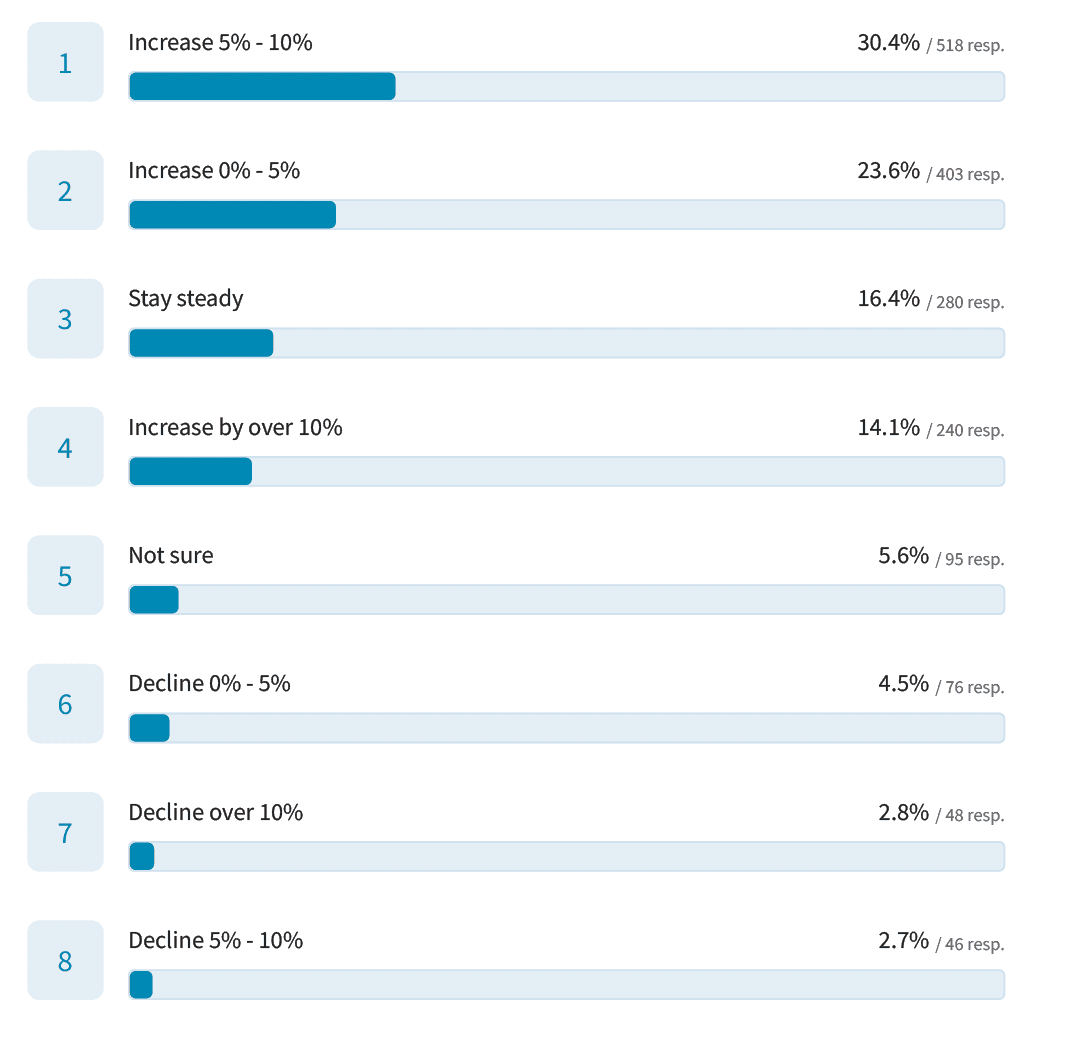

68% of respondents see property values rising in the next year.

Last year only 45% of respondents thought property values would rise in 2021.

Here’s the response when we asked what will happen to property values in 2022:

Has the pandemic changed your strategy or approach to property investing?

While 18% of the respondents were a little more cautious due to the current economic climate, the vast majority of investors (65%) are not changing their approach to property investment.

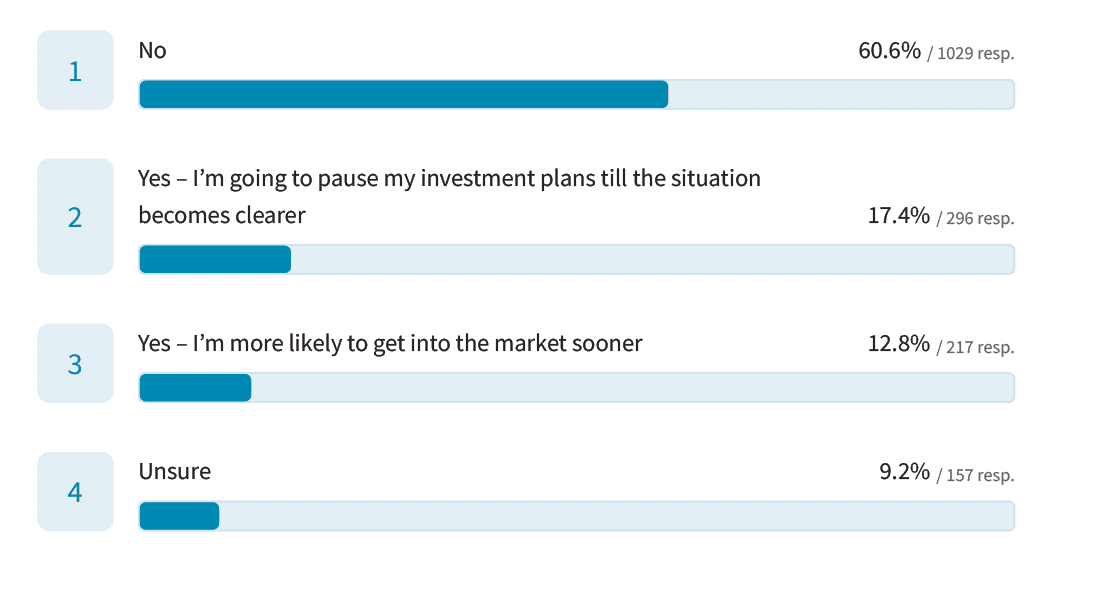

Has the pandemic impacted your immediate investment plans in the next 12 months?

While 17% are pausing the investment plans until the situation became clearer, the majority of respondents are not going to change their plans and 13% are going to take advantage of the current climate to enter the market sooner.

What type of property are you planning to buy?

Clearly off the plan properties are out of favour with respondents keen to buy established properties and in particular those with the ability to add value through renovation or development.

While only 6.8% requested a mortgage repayment holiday from their lenders (10% last year), 19.5% of the respondents had received a request for a rental reduction or holiday because of COVID-19 from the tenants – down from 24% last year.

Some other interesting results:

Some other interesting results:

- 62.6% of the respondents believe this as a good time to lock in interest rates, suggesting that most felt the next move in interest rates will be up. Last year 47% of the respondents thought it was time to lock in interest rates

- 26.7% of respondents are finding the recent tighter lending criteria impacting their ability to purchase another property.

Interestingly this is considerably lower than the last few years (2020 – 38%; 2019 – 42%; 2018 – 50%; 2017- 48%; 2016 – 46%) suggesting that banks’ lending criteria are easing a little.

- Difficulty with accessing more finance was the biggest concern of these property investors

The Bottom Line

The fact that respondents to this survey already subscribed to Property Update or Yahoo Finance meant they were a captive audience of people already interested in the property.

When asked for their combined family income 4% earned less than $50,000 while 34% earned more than $200,000 but the bulk earned a combined family income between $100,000 and $200,000.

83% owned at least one investment property, but a wide spectrum of investors partook in the survey:

- 16.9% owned no investments

- 22% owned one investment property

- 18.8% owned two investment properties

- 13.2% owned three investment properties, and it went all the way up to

- 4.8% owning 10 or more properties

And clearly, these investors took a long-term view because while over half the respondents planned to buy an investment property in the next year, they had realistic expectations about lower capital growth in 2022.

However, our survey shows that Australian property investors focus on long-term capital growth, rather than cash flow and many are looking for a property that has the potential to add value, rather than waiting for the market to do the heavy lifting.

Investors will still face a number of hurdles with the economic challenges facing Australia, yet few have changed their long-term plans due to COVID-19.

Click here to read the full survey results.

from Property UpdateProperty Update https://propertyupdate.com.au/australian-property-investors-are-more-cautious-about-the-future-of-property-in-2022/

“The luxury market has continued to power full steam ahead in 2021

“The luxury market has continued to power full steam ahead in 2021

APRA is concerned that because of our recent strong housing market activity, home loan sizes are increasing faster than incomes, potentially increasing the debt load for new borrowers.

APRA is concerned that because of our recent strong housing market activity, home loan sizes are increasing faster than incomes, potentially increasing the debt load for new borrowers.

This means that when the number of new investors starts to fall, they can suddenly crash.

This means that when the number of new investors starts to fall, they can suddenly crash.

Home loan data allows us to identify who is buying and therefore driving demand for property.

Home loan data allows us to identify who is buying and therefore driving demand for property.

Pre and early retirement moves fast-tracked across the rest of Queensland

Pre and early retirement moves fast-tracked across the rest of Queensland