It’s a bold statement, but it’s true.

For some of you who are reading this right now, 2021 is absolutely the worst possible time you could consider buying a property.

In fact for these people, moving forward with a real estate purchase this year would have the potential to cripple them financially, not just now but well into the future .

Sounds dramatic, right?

And I’ll give you 9 reasons why this could be the worst time to buy property in a moment… but here’s the truth.

This statement rings true in 2021.

It was also true last year.

And the year before that.

And in 2015, 2010, 1985, 1972…

The reality of real estate is that…

There is no “best” time or “worst” time to buy property

Here’s why…

Property investment is a process, not just event.

So rather than just talking about going out and buying a property in 2021, the right time for you to consider investing is when you have all your ducks in a row.

This means you have:

- a strategic property plan, so you know where you’re heading and what you need to do to achieve your financial goals,

- set up the right ownership structures to protect your assets and legally minimise your tax,

- a robust finance strategy with a rainy day buffer in place to buy you time

Of course, for some 2021 will be a great year to invest, but in a moment I’ll explain why that will not be the case for others.

However, it’s likely that you’ve heard me talk about the drivers of property price growth over the years.

There are so many things that determine a property’s price performance and growth trajectory, many of which are well outside of your control, and some which also have nothing to do with the property itself.

These include, but are not limited to:

- The economy – the performance and state of the broader economy impacts people’s ability to buy and sell the property as well as …

- Consumer Confidence – when people feel comfortable about their financial situation and their future job prospects they are more likely to make big purchases like moving home or buying an investment property.

- Employment levels – if the community at large is experiencing high levels of unemployment, then fewer people can afford to pay a mortgage, which reduces demand for property

- Government policy – aspects to do with tax, depreciation and homeownership grants will work to boost or reduce demand for property, particularly new property in recent years, which is where the federal government’s primary agenda has been.

- Population growth – or household formation to be more exact, as when more people moving into an area this equals more demand for housing, whether it’s to buy or rent.

- Local Demographics – things like average incomes, average age, household structure, crime rates, and employment opportunities.

- Supply – The basic economic principle of supply and demand is a fundamental property market driver of price growth.

- Availability of credit – property investment is a game of finance with some houses thrown in the middle, but even owner-occupier demand is very much driven by the availability of finance and the cost of money, in other words, interest rates.

Now, as a result of these factors – which are by no means an exhaustive list, but they give you a general indication of some of the major influences on property prices – our property markets move through cycles, from booms to busts and back again.

And currently, it looks like we’ll have a combination of multiple growth drivers to give investors a once-in-a-generation window of opportunity to take advantage of the upturn stage of a new property cycle.

Here are some of the indicators suggesting that 2021 will be a great year for property investors: –

- Consumer confidence has been continually improving, as has business confidence

- COVID numbers are very low, and the prospects of a robust vaccination program is excellent,

- Our economy is improving faster than many expected – we’re in for a V shape recovery.

- Auction clearance rates were consistently strong in the last few months of 2020, not just in the two big auction capital of Melbourne and Sydney but around Australia, and are starting 2021 on a very positive note.

- More buyers and sellers are in the market and transaction numbers have increased considerably.

- At the same time, the banks are keen to write new business – another positive for our housing markets.

- Bank loan deferrals have been falling – there’s no chance of an avalanche of forced mortgagee sales as many were worried about.

- The latest rate cut and the “guarantee” of rates remaining low for at least 3 years, will give home buyers and investors confidence

- Moving forward further jobs creation, consumer confidence and business confidence (leading to spending and employment) will underpin our housing markets.

So why could this be the worst time to invest for some people?

Please let me explain with an example…

Between 2016 and 2018, Sydney and Melbourne property values soared allowing those who owned properties in our two big capital cities to amass small fortunes along the way.

But it’s important to know that just because “Sydney boomed”, that doesn’t mean that ALL of Sydney housing boomed.

It means that overall, the majority of properties across the city experienced an increase in value.

However, there are always some areas, pockets, streets, and individual houses that perform better or worse than the average.

For example, the value of the apartments in many of the high-rise, Legoland towers around Sydney languished as concerns about structural integrity, following the Opal Towers debacle tarred all new apartments with the same brush.

Of course, the concerns raised by Covid19 only added to this.

Let me give you a different example

Let’s say a couple owned a property in a sought-after Sydney suburb in 2017.

They had purchased in 12 months earlier for $1.55m.

It’s right in the middle of a booming property market and sadly, the couple split up.

It’s right in the middle of a booming property market and sadly, the couple split up.

It’s a messy and contentious divorce, and both parties want to sell the home as quickly as possible so they can move on.

They also don’t want any looky-loo neighbours snooping through their home every weekend, and they don’t have the energy or appetite for a big, public marketing campaign.

So, they engage a real estate to sell the home privately/off-market.

It reaches fewer potential buyers and drives less competition, but they secure a buyer within a week.

They sell the property for $1.6m in a hasty settlement and move on.

Had they taken the property to the open market – say, an auction – and a number of would-be buyers fell in love with the property, they could have sold for more money.

But their circumstances dictated a swift sale, so they accepted the price they got and moved on.

It could be the case that one street over, a couple own very similar property.

They are planning to move in with their parents for six months while they build their next property, so they have no deadline or timeline pressures and they’re happy to wait for the right buyer to come along.

They are planning to move in with their parents for six months while they build their next property, so they have no deadline or timeline pressures and they’re happy to wait for the right buyer to come along.

They list their home for auction, pay for an expensive but very high-profile marketing campaign, and achieve a final sale price of $1.825m.

Two similar homes, two very different outcomes.

Neither is “right” or “wrong”, and this is the infuriating truth of real estate: there are no “definites.”

Just a series of educated guesses and informed choices, which – with the right expert guidance – can lead you towards making profitable decisions for your future.

When it comes to deciding the right time to buy or sell, at the end of the day, it’s our own personal situation as much as external factors that influence the best course of action we should take.

The fact is, any time could be the worst time for you personally to buy a property… or it could be the best time to buy

It truly depends on your own goals, budget, timeline, risk profile, and circumstances as to whether 2021 is a good time to buy.

If you’ve just lost your job or your income is insecure in the current economic climate, then yes, this could be a risky time to commit to a mortgage; in fact, you’d struggle to get a loan.

However, if you’re financially stable and have a deposit ready to go, then some might argue that with 2% mortgage rates and prospects of strong house price growth, 2021 could be the property buying opportunity of a lifetime.

What’s ahead for our property markets for 2021?

That’s a common question people are asking now that our real estate markets are up and running again.

We’ve worked our way through many of the effects of the Coronavirus Pandemic and out of Australia’s first recession in 30 years.

I guess many property investors and homebuyers are looking for property market prediction or forecasts – they’re wanting to know what’s going to happen to real estate prices moving forward.

Well forecasting is difficult – especially about the future – but it really looks like all the pieces to the property puzzle are falling into place and our property markets will perform strongly in 2021.

In my regular blogs and podcasts last October (2020) I announced that Australia’s property markets had turned the corner after being put on pause by the coronavirus induced lockdowns which caused “the recession we made us have.”

But now it’s official, property markets are performing strongly.

In fact, some commentators are even calling it a “Boom”, with property values rising as more Australians are looking for a new home or to upgrade their homes at a time when there are fewer properties on the market.

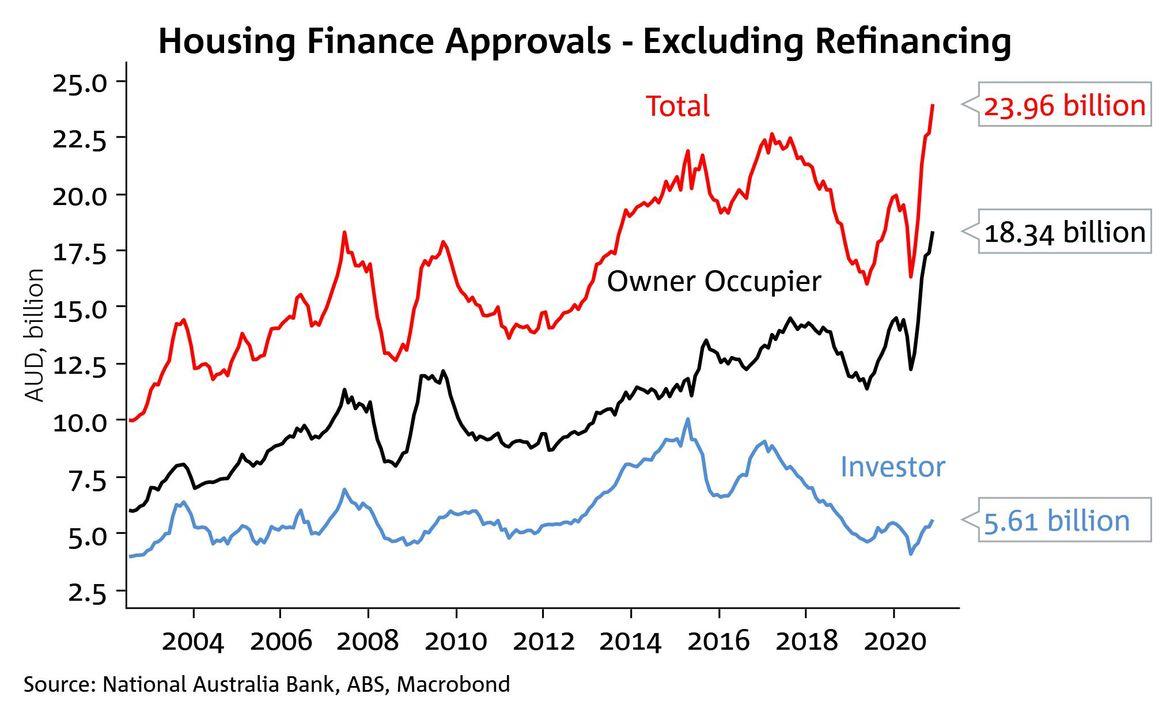

One of the “leading indicators” our research team at Metropole watch carefully is home loan activity.

The most recently released ABS finance data reported that the value of new home loans taken out in November set a new national record.

Property investment is a game of finance with some real estate thrown in the middle, and when finance flows more freely and people take out loans before they commit to purchasing a property, then next logical result is rising property prices.

Some of the other positive factors are:

- Australia’s economy is recovering faster than most expected

- Unemployment is falling as many new jobs are being created – in fact, most of the jobs lost due to Covid have been restored

- Consumer confidence is rising and more people than ever see this as a great time to invest in property or upgrade or buy their first home

- At the same time as more buyers are entering the market, the number of properties for sale in Australia is beginning to dry up

- First home buyers are back in the market taking advantage of the mini incentives offered to them

- We are not going to fall off the fiscal cliff many were worried about. The mortgage time bomb isn’t going to explode as 80% of those who deferred their mortgages have now started to repay them.

NOW READ: The pieces to the property puzzle are falling into place. Here’s what’s ahead for property in 2021

Sure there are problems in some of our rental markets and certain sectors of our real estate markets are still suffering, but having invested in property for almost 50 years I’ve found that whenever there has been an economic threat, recession, interest rate spike, or credit squeeze, the residential markets always bounce back, usually more quickly than projected, demonstrating the resolve of the Australian community to maintain its embrace of real estate and homeownership.

Here’s 9 reasons why 2021 could be the worst time for you to buy an investment property

- You are buying a property to pay less tax –

Don’t be lured into buying secondary properties that offer high depreciation allowances for excessive negative gearing.

These new properties tend to come at a premium price, and rarely deliver capital growth for many years.

In my mind negative gearing is not an investment strategy – it’s for short-term funding strategy which only makes sense when used to purchase high growth investment great properties.

These tend to be established houses, townhouses, or apartments in desirable streets in top locations in the middle ring suburbs of our three big capital cities. - You are driven by FOMO – fear of missing out.

Sure our property markets are moving ahead, and of course, it’s human to become emotional when considering buying a home or an investment property.

But investing emotionally leads to bad investment decisions – it’s exactly this type of emotion and that makes investors fall prey to property marketers and spruikers who will offer you a way to get rich quickly. - You want to get rich quickly.

Property investing is a long-term endeavor.

I’ve found it takes the average property investor 30 years to become financially free. - You don’t really understand how property investment works

Many people mistakenly believe they understand property investment because they own a house or have lived in one.

So they end up buying a property close to where they want to live, where they want to retire or where they holiday.

Again, these are emotional reasons to purchase a property rather than selecting based on sound investment fundamentals.

On the other hand, successful investors have formulated a sound investment strategy that suits their risk profile and helps them achieve their long-term goals and one which has stood the test of time. - You’re not financially fluent.

I found many investors are looking to invest in property to help increase their cash flow, but if they do not have the financial discipline and cash flow management skills required, taking on the extra debt of an investment property only compounds their problems. - You’re looking for a multi-purpose property

If you are buying a property with the aim of creating wealth, but it also has to be your future home or a part-time holiday home, or somewhere to retire in the future; then you’re probably wanting too much for that one little property to achieve. - Your finances are not in order

Property investment is a game of finance with some real estate thrown in the middle.

To get into property you should have a stable job, profession, or business with a steady income and need to be attractive to the banks so they lend you money plus you should have sufficient stashed away in a financial buffer to see you through the inevitable rainy days ahead. - You don’t have enough money (yet!)If you can’t afford an investment-grade property, either because you haven’t saved a sufficient deposit or you can’t service the loan repayments, then rather than buying a secondary property, in my mind it’s better that you wait and buy an investment-grade property.

- You are trying to time the market or find the next hotspot.

Sure property markets move in cycles and it would be great to buy near the bottom or find a location that will be the next hotspot, but the landscape is littered with investors who tried to time the market and failed.

Instead, the right time to buy real estate is when your finances are in order and you’ve got the ability to purchase an investment-grade property.

Remember there is no one property market in Australia so there will always be opportunities somewhere.

Now is the time to take action and set yourself for the opportunities that are currently presenting themselves as the market moves on in 2021

If you’re wondering what will happen to property 2021 you are not alone.

You can trust the team at Metropole to provide you with direction, guidance and results.

In challenging times like we are currently experiencing you need an advisor who takes a holistic approach to your wealth creation and that’s what you exactly what you get from the multi award winning team at Metropole.

If you’re looking at buying your next home or investment property here’s 4 ways we can help you:

- Strategic property advice. – Allow us to build a Strategic Property Plan for you and your family. Planning is bringing the future into the present so you can do something about it now! This will give you direction, results and more certainty. Click here to learn more

- Buyer’s agency – As Australia’s most trusted buyers’ agents we’ve been involved in over $3Billion worth of transactions creating wealth for our clients and we can do the same for you. Our on the ground teams in Melbourne, Sydney and Brisbane bring you years of experience and perspective – that’s something money just can’t buy. We’ll help you find your next home or an investment grade property. Click here to learn how we can help you.

- Wealth Advisory – We can provide you with strategic tailored financial planning and wealth advice. Click here to learn more about we can help you.

- Property Management – Our stress free property management services help you maximise your property returns. Click here to find out why our clients enjoy a vacancy rate considerably below the market average, our tenants stay an average of 3 years and our properties lease

from Property UpdateProperty Update https://propertyupdate.com.au/worst-time-to-buy-property/

No comments:

Post a Comment