Are you considering buying an off-the-plan investment property?

Please think again and turn the other way!

There are just too many risks involved in this sector of the market.

Now with our property markets booming around Australia and FOMO (fear of missing out) kicking in for many beginning investors, I know some are are thinking- “I’ll put a small amount down as a deposit today and settle in a few years time when all this Coronavirus “stuff” is over” and they’re hoping to turn a relatively small deposit into a substantial profit, all while avoiding those nasty holding costs.

Other investors are tempted to buying off the plan properties being enticed by the advertising hype of stamp duty savings, depreciation allowances and so-called “cheap” prices.

But while buying Off The Plan has rarely been a good investment strategy, this is the riskiest investment strategy in the current market and one to be avoided.

What are these new risks to off-the-plan properties?

While there are already major risks associated with this type of investment due to a number of factors, including oversupply, the changes to our attitudes of how we want to live post COVID-19 means fewer people will be keen to live squashed in with hundreds of other residents in poor quality apartments in Lego Land Towers.

This includes both owner-occupiers and tenants.

This means vacancy rates will be higher in this type of building – in fact, one in five properties are vacant in many of the CBD apartment towers.

This is a poor recipe for rental and capital growth.

Add to this the recent concerns about the well-publicised structural integrity issues in Opal Towers and many other buildings which have dampened investor confidence in the new apartment market and falling apartment values and you can start to see what I’m getting at.

NOW READ: Some high rise apartments will be the slums of the future

So does buying off the plan ever make good investment sense?

The answer is usually no.

While a few investors have made money buying off the plan, the road is littered with much more who have regretted their purchase.

Frequently they’ve found the value of their property on completion is considerably less than they paid.

There are many other issues with buying off the plan, but before I explore them let’s first understand why projects are marketed this way.

While developers know they can get a better price for a completed property that buyers can see and touch and feel, today the lenders who are going to fund the construction of the project insist a substantial proportion of units be pre-sold to ensure the viability of the project is underwritten.

Obviously, the banks expect the developer to make a reasonable profit margin – and so they should.

This is built into the final price as are the substantial marketing budgets which cover the cost of those full-page ads in the papers and expensive glossy brochures produced for the project.

Add to this the generous selling commissions given to project marketers and incentives offered to financial planners and you can understand why the initial selling cost is inflated.

Remember, there is no such thing as a “free lunch.”

If 10 -15 per cent of the project’s budgeted selling price is spent on marketing and selling costs, then the buyer must pay for this.

As the completion date for many high-rise inner-city projects maybe a few years away the inflated price can be buried in advertising hype such as “buy at today’s prices” and settle in two years.

The developers are counting on the fact that the longer the settlement period, the less chance you have of knowing if the final price will represent good value for money.

Looking back, many investors who have bought off the plan over the last decade found that the price they paid was way too high and on completion, their properties were valued at considerably less than their purchase price.

Here’s a few reasons I would steer clear of buying off the plan:

1. Too many fingers in the pie

I’ve seen far too many off-the-plan properties sold with large commissions built-in for middlemen, marketing budgets, and salespeople, meaning the investor pays well over its true underlying value.

Don’t be lulled into a false sense of security just because you’ve been told a number of pre-sales have already occurred.

Many of these apartments have been sold to naive investors by introducers.

These range from project marketers to salespeople disguised as mentors at “free” seminars, to mortgage brokers, financial planners, and accountants who are paid “kick-backs” often in the range of 8% of the purchase price.

You’re also likely to find many of these properties have been purchased at inflated prices by overseas buyers who are unable to buy established properties, have little knowledge of the local markets, and have unique motivations for buying a property in Australia such as a desire to emigrate in the future or place their money in a more stable country.

Of course, valuers are familiar with these practices and that’s why, on completion, most of the plan properties value in at considerably less than the contract price.

2. The banks won’t buy it!

Given that most loan approvals are only current for three months, obtaining a formal pre-approval for an off-the-plan purchase is a waste of time.

The problem is, currently we have 4 big banks in Australia and they each have a policy restricting their exposure to anyone building; most won’t lend to more than 15% of the properties in a large complex.

This means that if there are 100 apartments in the building and you are the 16th person to approach the bank when the building is completed, they may decline your application and you’ll have to go chasing finance elsewhere.

And if they do lend for your purchase you may find because of the inner city postcode of your new high-rise purchase, they will lend at lower loan to value ratios, meaning you need a bigger deposit.

By the way… some investors who buy off the plan won’t be able to settle and will need to sell their property at whatever price they can achieve.

Unfortunately, that’s what the banks will value your property at – the going selling price on completion – not what you paid for it.

Combine this with a lower loan to value ratio and you’re likely to need an even bigger deposit than you initially thought.

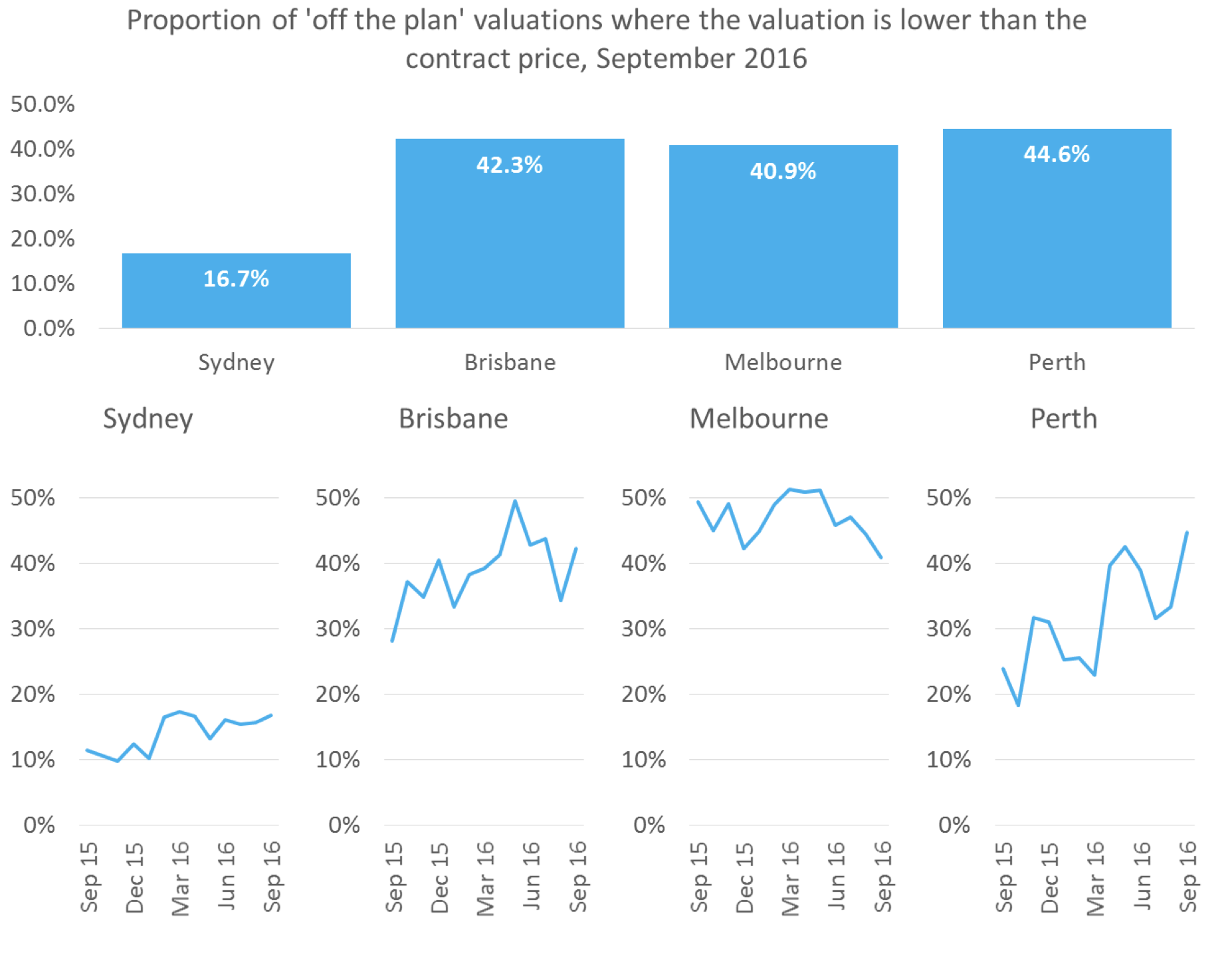

Now the following graphic from Corelogic should be enough to put you off buying off the plan.

It shows the huge percentage of properties bought off the plan where, on completion, the valuation is lower than the contract price:

3. Low land to asset ratio

Remember that old investment rule; land appreciates while buildings depreciate?

If you go by the book, you should aim for the highest land to asset ratio possible and aim to get as much valuable land under your apartment as you can.

However, the developer wants the opposite and squeezes as many apartments on the site as they possibly can.

So essentially, the interests of the developer and you – the investor – are in direct opposition.

4. No scarcity

This is an important factor limiting resale value as these properties have little owner-occupier appeal.

Not only will most of the new apartment blocks have many similar dwellings (in size, layout, and style); chances are there will be many similar apartment blocks in the surrounding neighbourhood.

5. Investor imbalance

Most off-the-plan developments are sold to investors.

This means you end up with a building occupied by far more tenants than homeowners.

The fact is owner-occupiers tend to be far more careful when it comes to maintaining the building and enhancing the development’s long-term capital value.

By the way…it’s not much fun going to a body corporate meeting full of investors who are not keen on spending (or simply don’t have) money to maintain the building.

6. Too many too soon

Currently, there is a significant oversupply of new apartments in some of our capital cities’ CBD’s and this glut of properties driving  down prices poses a problem for investors relying on the value of their property to increase by the time it reaches completion.

down prices poses a problem for investors relying on the value of their property to increase by the time it reaches completion.

An oversupply of properties for sale and for rent means your investment will lack scarcity value, one of the factors that I look for to help increase the value of my properties.

Of course, the various landlords will be in competition with each other for tenants and I’ve seen this quickly turn into a race to the bottom.

Sure many aspiring investors think: “Oh, but the developer is giving us a rental guarantee”.

This means just means that the developer is nominating a (likely inflated) rental promise and matching any differential for a year or two and in the meantime inflating the price you pay to cover his risk.

And things will get worse…

With many investors unable to settle on their off the plan purchases because the banks have tightened their lending criteria – and this doesn’t just apply to foreign investors, locals are having real trouble too – there will be a glut of unsold properties hitting the market as developers try and unload their stock.

7. Developer dilemmas in off-plan purchases

Did you know that many of the off-the-plan projects currently being marketed won’t get out of the ground?

Sure you’ll get your deposit back, but it means you’ve lost precious time with your money not working in the market.

On the flip side, when the developer completes the project don’t be surprised if they have made some amendments to the floor plans or substituted different finishes or fittings.

While they have the right to do so in the contract, you’ll usually find the changes are in their favour and not yours.

You see…developers generally insert a clause in an off-the-plan sales contract that allows them to vary the property within a certain percentage if they chose to do so, and without the buyer having any recourse.

8. Rental guarantees are not as solid as you might think

Often developers will offer a rental guarantee to entice investors who might be more focused on their cash flow and worried about vacancies.

The problem is you pay for these rental guarantees in the purchase price, which is another cost that inflates the apartment’s already premium price.

And once the guarantee expires, the rental income reverts back to the going market rate which is usually lower than that offered in the guarantee.

9. Excessive Owners Corporation fees

Generally, owner’s corporation levies are high in these buildings diminishing your rental yields.

And don’t necessarily believe the fees quotes by the project marketer as these are usually unknown and often underestimated at the time of sale.

Remember many of these buildings require expensive upkeep of their lifts, grounds, gardens, pools, and gyms.

Then give it a few years the ongoing maintenance costs start creeping in with the need to upgrade, painting and replacing of items.

What lessons can we learn from this?

Some of these problems could be avoided by buying from developers with a good track record and buying in buildings in prime locations, as there always seems to be a bigger demand for units in these buildings.

Also while buying off the plan has the potential for capital growth, if you bought a completed property it should also grow over the same 12 to 18 months you were waiting for your off the plan purchase to settle.

With a two or more year time-frame for the completion of most high-rise projects, it is very difficult to predict what the future will hold so I feel you should receive a sizeable discount for all the uncertainty of buying off the plan.

There is uncertainty about what the property markets will be like on completion, what will the interest rate be then, will the standard of finish be as good as in the display unit or will the developer have cut corners, and what will be built in the future alongside, behind, or in front of the project.

What appears to be a great view today may be totally blocked out in two years’ time.

To cover all these uncertainties, surely you should be buying at a substantial discount, but in reality, you are usually paying a premium – therefore giving your developer your first couple of years’ capital growth (and he doesn’t deserve it).

What’s the alternative to buying off the plan?

I prefer buying established apartments and to ensure I buy a property that will outperform the market averages I use a 6 Stranded Strategic Approach. I buy:

- A property that will appeal to owner-occupiers (because they’re the ones that push up property values.)

- Below its intrinsic value – that’s why I avoid new and off-the-plan properties, which come at a premium price.

- In an area that has a long history of strong capital growth and which will continue to outperform the averages.

- I only buy properties with a substantial land to asset ratio

- I look for a property with a twist – something unique, special, different or scarce about the property, and finally

- A property where I can manufacture capital growth through refurbishment, renovations or redevelopment.

By using a strategic approach I minimise my risks and maximise my upside.

Each strand represents a way of making money from property and combining all five is a powerful way of putting the odds in my favour. If one strand lets me down, I have three or four others supporting my property’s performance.

Now is the time to take advantage of the opportunities the current property markets are offering.

Sure the markets are moving on, but not all properties are going to increase in value. Now, more than ever, correct property selection will be critical.

You can trust the team at Metropole to provide you with direction, guidance, and results.

Whether you’re a beginner or an experienced investor, at times like we are currently experiencing you need an advisor who takes a holistic approach to your wealth creation and that’s exactly what you get from the multi award-winning team at Metropole.

We help our clients grow, protect and pass on their wealth through a range of services including:

- Strategic property advice. – Allow us to build a Strategic Property Plan for you and your family. Planning is bringing the future into the present so you can do something about it now! Click here to learn more

- Buyer’s agency – As Australia’s most trusted buyers’ agents we’ve been involved in over $4Billion worth of transactions creating wealth for our clients and we can do the same for you. Our on the ground teams in Melbourne, Sydney and Brisbane bring you years of experience and perspective – that’s something money just can’t buy. We’ll help you find your next home or an investment-grade property. Click here to learn how we can help you.

- Wealth Advisory – We can provide you with strategic tailored financial planning and wealth advice. Click here to learn more about we can help you.

- Property Management – Our stress-free property management services help you maximise your property returns. Click here to find out why our clients enjoy a vacancy rate considerably below the market average, our tenants stay an average of 3 years, and our properties lease 10 days faster than the market average.

from Property UpdateProperty Update https://propertyupdate.com.au/buying-off-the-plan/

No comments:

Post a Comment