Owner occupiers have been the primary driver of the housing market rebound, comprising 76% of all new home loans over the twelve months to March 2021 compared with the decade average where owner occupiers have comprised a smaller 65% of demand; but the mix of housing activity is starting to change as investors become more active.

The past six months has seen the value of investor loans increase by 48.1% while the value of owner occupier loans is up a smaller 29.7%.

The March quarter alone saw the value of investment lending for housing surge by 28.7% while the value of new owner occupier home loans was up a much smaller 12.4%.

On an annual basis, the growth in the value of owner occupier lending (+55.6%) is now roughly on par with the lift in investor loans (54.3%) as investors play catch-up.

On an annual basis, the growth in the value of owner occupier lending (+55.6%) is now roughly on par with the lift in investor loans (54.3%) as investors play catch-up.

Despite the rise in investor lending, investment loans comprised only 25.9% of the value of new mortgage commitments in March, up from a recent record low of just 23.1% in January this year, but well down on the decade average and the historical highs recorded in 2015.

Historically, the share of investor activity peaked at 45.9%, shortly after macroprudential measures were announced by APRA in December 2014.

The 2014 measures placed a 10% speed limit on investment credit growth.

Although the share of investor lending staged a temporary bounce back in 2016, investor activity turned due to a second round of credit tightening in 2017, which focused on reducing interest only lending.

Coupled with a more cautious lending environment during and after the Royal Commission, the share of investors in the market trended consistently lower until February this year.

Investor activity remains below average across every state and territory, ranging from just 13.3% of mortgage demand in the Northern Territory to 31.5% of demand across New South Wales.

The loan commitments data shows investor demand remains concentrated in New South Wales with most of this activity likely to be concentrated within the Sydney region.

New South Wales has historically attracted the largest share of investors, with this group of buyers averaging 41.4% of mortgage demand over the past ten years and in March 2021, New South Wales was the only state where investors comprised more than 30% of mortgage demand.

The concentration of investors in New South Wales may seem a little counter intuitive.

The concentration of investors in New South Wales may seem a little counter intuitive.

Sydney is the most expensive capital city by some margin, implying the financial commitment is more significant than other regions.

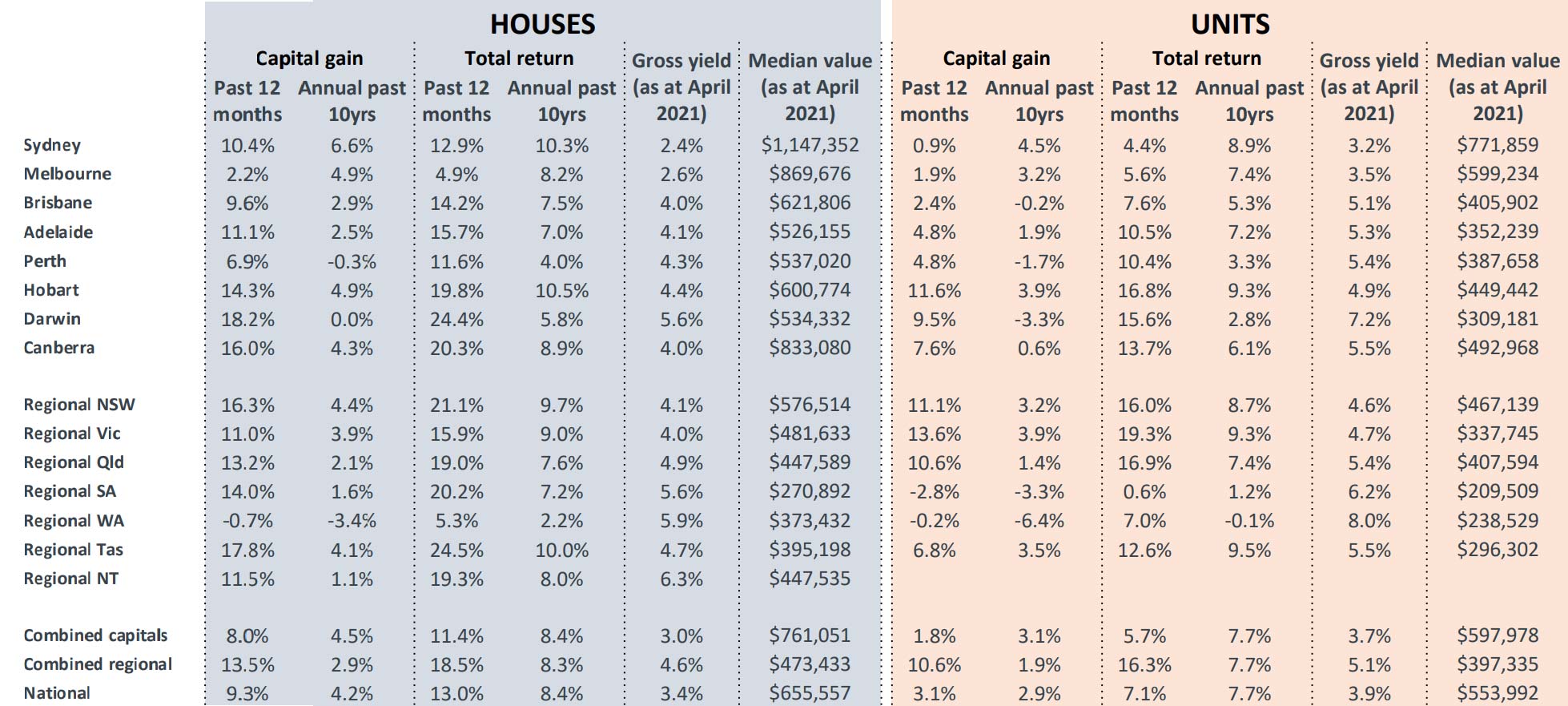

Where Sydney stands out is capital gains; Sydney has the highest average annual rate of capital gains over the past decade with house values averaging a 6.6% rise each year and unit values averaging 4.5% per annum.

With most investors focused on capital gain rather than rental return, this track record of growth might help to explain the popularity of Sydney amongst investors.

Over the past 12 months, Darwin has recorded the most significant rate of capital gain, with house values up 18.2%. Regional Tasmania (17.8%) and Regional New South Wales (16.3%) come in a close second and third.

Across the unit market, the swiftest rise in values has been in Regional Victoria (13.6%) and Hobart (11.6%).

For investors more focused on cash flow opportunities, the higher yielding markets may be more attractive.

The highest capital city gross rental yields can be found in Darwin (5.6%), Hobart (4.4%), and Perth (4.3%) for houses, while gross yields for units are highest in Darwin (7.2%), Canberra (5.5%) and Perth (5.4%). Yields are generally higher across regional markets, with Regional Northern Territory (6.3%) and Regional Western Australia (5.9%) recording the highest gross yields for houses.

Regional WA also stands out with the highest gross yield for units at 8.0%.

The total return, which provides a measure of the annual capital gain plus annualised gross rental return, highlights the areas that have provided the best overall investment returns.

Over the past twelve months, regional Tasmania (24.5%) and Darwin (24.4%) have provided the highest total returns for houses amongst the broad regions of Australia.

For units, the strongest overall returns over the past year have been in Regional Victoria (19.3%) and Regional Queensland (16.9%).

Of course, past performance is not a guarantee of future performance.

In fact, the best investment options may be those markets that have underperformed over previous cycles, providing a more affordable environment and generally higher rental yields.

Demographic factors, which have changed significantly over the past twelve months, will also play a role.

Overseas migration is set to remain low for at least the next year, implying regions with strong interstate and internal migration rates will have a higher level of housing demand.

South East Queensland, Perth and regional areas of Victoria and New South Wales are all showing a positive demographic trend.

Economic conditions are also important.

Regions with a diverse economic base are likely to show less risk relative to areas with shallow economies.

Trends in job growth, employment rates, and capital investment such as significant infrastructure spending are also critical for picking areas ripe for investment.

Key housing market statistics by broad region as at April 2021

from Property UpdateProperty Update https://propertyupdate.com.au/are-investors-barking-up-the-wrong-tree/

No comments:

Post a Comment