Sydney and regional NSW have been among the ‘top performing’ housing markets through the start of 2021 in terms of value change.

This follows a peak-to-trough fall in Sydney values of -2.9% between April and September of 2020, and a dip of just -0.1% in May 2020 across regional NSW.

Through the calendar year to April 2021, Sydney dwelling values have risen 9.3%, and regional NSW dwelling values are up 9.0%.

Both dwelling markets are at record highs.

Within these regions, growth has largely been driven by the ‘high-end’ of the market.

This is reflected in CoreLogic tiered hedonic indices, which show the top 25% of Sydney values have increased 12.0% compared with a 5.4% rise at the ‘low’ end of the market from the start of 2021 through to April.

It is also reflected regionally, where quarterly increases have been positively correlated with median dwelling values.

With such rapid growth rates across already expensive markets, affordability constraints are likely to become most pressing across Sydney.

When adjusted for the median dwelling value, the rate of increase since the start of the year equates to a rise of over $80,000 in the median Sydney dwelling value, and almost $46,000 for the rest of NSW.

The uplift is also very broad-based. The only SA3 market across NSW recording a loss in the three months to April were Liverpool units, where values declined -0.8% in the period.

Sales activity has remained strong across the state.

In the twelve months to April, CoreLogic estimates there were 96,505 transactions across Sydney, up 18.0% from the previous year.

This included a 13.2% uplift in unit sales and a 21.6% lift in house sales.

Regional NSW saw an even more impressive uplift in sales volumes, with a 32.6% increase in transactions over the 12 months to April, totaling 71,032 transactions over the year.

The rate of increase in sales across regional NSW was actually higher across the unit segment (34.2%) than houses (32.3%).

However, dwelling value growth in NSW did ease over the month of April (2.4%) compared with March (3.5%).

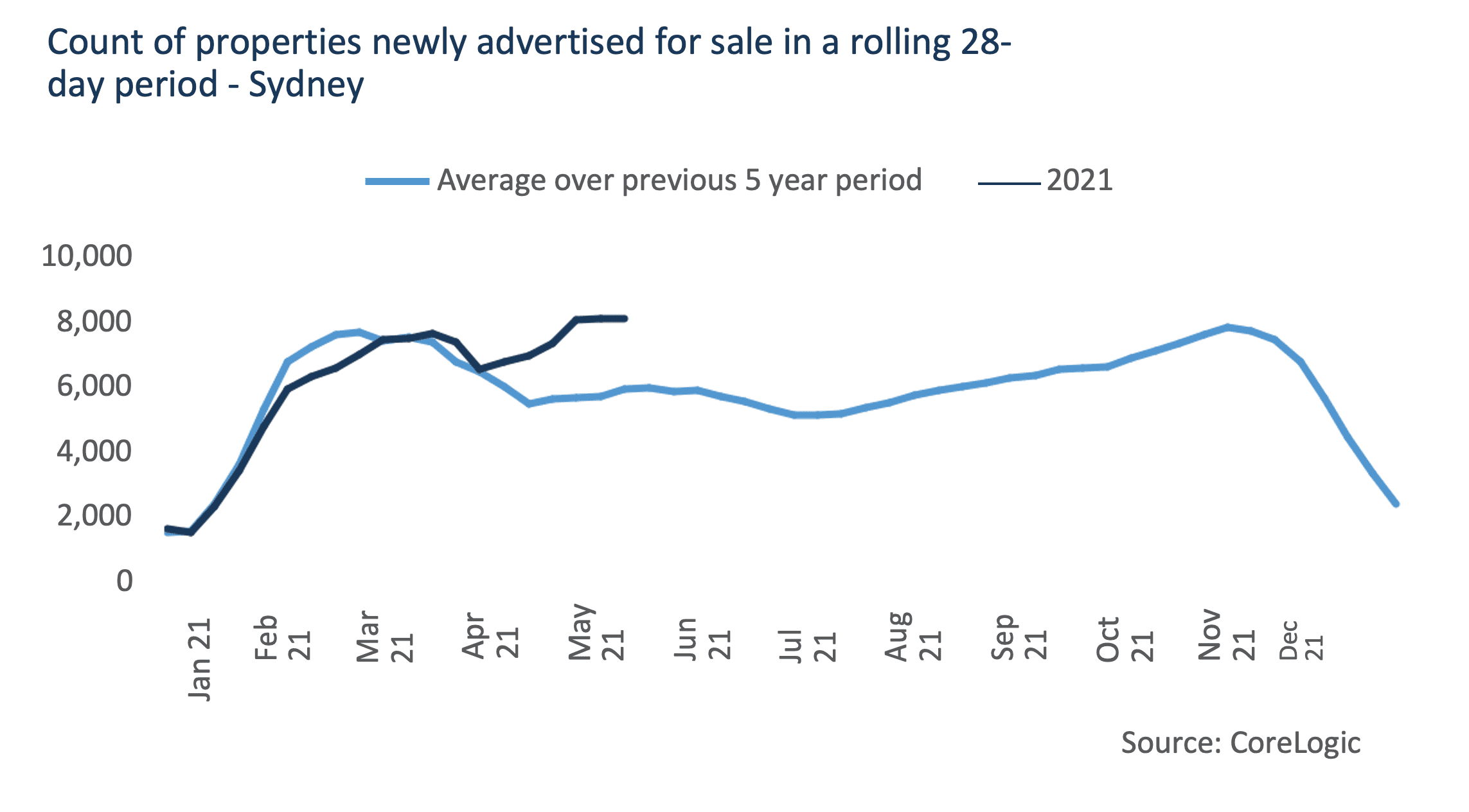

One sign of a potential easing in conditions across the NSW housing market is a recent surge in properties newly advertised for sale.

This is particularly pronounced in Sydney, where the count of new listings added to the market increased from 6,974 in the four weeks to 18th of April, to 7,969 in the four weeks to 23rd of May.

The chart below shows the relative surge in supply this represents relative to previous years.

The markets with the biggest uplift in new listings over this period were the Sydney Inner City market (which saw an additional 105 listings), Campbelltown (with 80 additional listings), and Warringah (with 61 additional listings over the period).

The increase in listings is most likely a mix of vendors responding to strong selling conditions, though ongoing weakness in some rental markets may also be prompting an investment sale.

The momentum in the NSW housing market is largely the result of Australian monetary policy settings, alongside COVID-19 remaining well contained in the state.

Unlike Victoria, where social distancing has slowed the economic recovery and demand for inner-city housing, the industries impacted by stage 2 restrictions last year in NSW are now starting to benefit from pent-up demand for discretionary spending.

However, affordability constraints and a recent uplift in vendor activity may result in slower value increases for the second half of 2021.

NOW READ: Sydney property market forecast to grow strongly in 2021-2022

Editor’s Note: This is an extract of Corelogic’s Quarterly Economic Review

from Property UpdateProperty Update https://propertyupdate.com.au/sydney-property-market-trends-so-far-this-year/

No comments:

Post a Comment