Australia’s housing markets are entering very tricky territory as the return of major virus disruptions combine with what has been an extraordinary boom that is starting to run into affordability constraints.

According to the latest Westpac Housing Pulse report, telling whether underlying conditions are hot or cold is going to be exceedingly difficult in the coming months, particularly for markets that are essentially shut.

On balance, Westpac expects the situation to see a temporary loss of momentum rather than a correction – even in the most heavily impacted areas – and then a rapid snap-back once restrictions ease.

Restricted inspections and fewer properties for sale will mean some sub-markets will be susceptible to weakness in the near term, particularly where economic pressures are intense and the virus outlook uncertain.

However, “thin trading” also means low ‘on-market’ supply that could be a big issue once activity rebounds, especially given the way demand has already been running well ahead of new listings.

Sentiment-wise, Westpac believes that broader consumer confidence has taken a substantial hit but is holding up compared to last year’s major lockdown episodes – with vaccine availability providing key support.

So far, surging prices and stretched affordability look to be more important to the future of our housing market sentiment than COVID considerations.

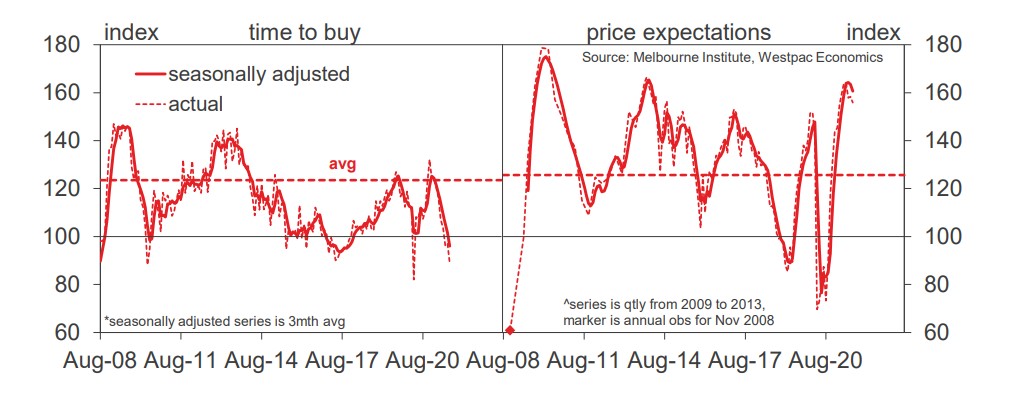

Consumer sentiment: housing

Consumer sentiment: jobs & risk

Westpac reports that the broad-based housing boom that began last year and accelerated strongly through the first half of 2021 has maintained robust momentum through the middle of the year but is entering a more uncertain phase.

Affordability is becoming stretched in most markets with many now encountering major virus disruptions as well.

The ‘delta’ outbreak is set to hit the wider economy hard near term with a steep fall in NSW and significant disruptions in Vic expected to see activity contract 2.6% in Q3.

Yet Westpac believes that a lift in vaccination rates should pave the way for some easing in restrictions in Q4.

Activity is expected to rebound 2.6% in the quarter and a further 2.4% in 2022’Q1.

For housing, COVID restrictions will again see major disruptions to market activity and building near term but both should stage strong rebounds once this ease according to Westpac.

The bank believes that property prices are expected to see a loss of momentum but outright declines look unlikely and growth should reaccelerate quickly once heavily affected markets reopen.

The housing-related sentiment reflects a mixture of forces: deteriorating affordability driving another sharp decline in assessments of time to buy’ price expectations still riding high; and the latest COVID shocks impacting mainly via a loss of confidence around jobs.

The combined signal remains positive for now but looks susceptible to slowing.

Residential property listings

The Westpac Melbourne Institute ‘time to buy a dwelling’ index dropped another 14.1% over the 3 months to August after a similar decline over the previous 3 months.

The index has now slumped by nearly a third from its November high of 132, August marking the second-lowest read since 2010.

According to Westpac the steep fall is a clear warning that deteriorating affordability is starting to weigh heavily on buyer sentiment amongst owner-occupiers.

In contrast, the Westpac–MI Consumer House Price Expectations Index is only marginally changed, a 4.9% decline over the last 3 months just a partial reversal of the 5.8% gain between February and May.

At 155.8, the Index nationally is still near historic highs.

Consumers registered a particularly sharp loss of confidence around jobs.

The Westpac Melbourne Institute Unemployment Expectations Index jumped 24.3% drop over the 3 months to Aug (note: a rise means more respondents expect unemployment to rise).

That said, jobs confidence was coming from a very strong starting point – the latest index read of 124.6 is still better than the long run avg read of 130.

The Westpac Risk Aversion Index remains elevated, easing marginally from 43.7 in March to 40.9 in June vs a long-run average of 14.8.

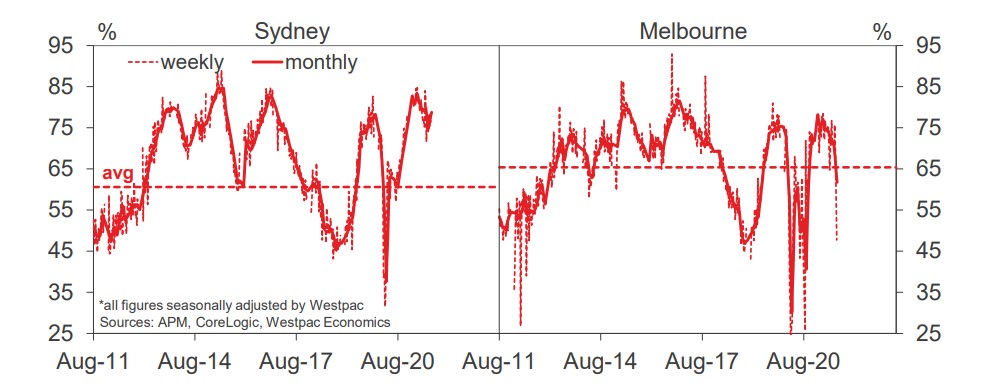

Auction markets are showing clear disruptions from the latest lock-downs with a sharp drop in volumes and a lift in pre-auction withdrawals.

That said, average clearance rates amongst those still going ahead are still relatively firm compared to last year’s lockdown lows.

Auction clearance rates

Listings have continued to trail sales by a long way and have dropped off sharply again during the latest lock-downs.

from Property UpdateProperty Update https://propertyupdate.com.au/the-current-state-of-play-in-our-property-markets-according-to-westpac/

No comments:

Post a Comment